Analytics

Why Markets Don’t Always React to Big News: A Baking Analogy

“It was already baked into the market reaction.” It’s something we at Marketplace, and other business news journalists, say when big news happens and the markets don’t seem to care.

But why not?

“I would say that the analogy to baking, when we talk about ‘baked in’ is pretty appropriate,” said Sasha Indarte, a professor of finance at the University of Pennsylvania’s Wharton School.

It’s a bit on the nose, but stay with us. Once all the ingredients are mixed together and the cake is in the oven, what’s going to come out when the timer goes off is already decided. It’s baked in.

The market works kind of the same way. Once news — or more accurately, anticipated news — is incorporated by stock market traders and other economic decision-makers, the news isn’t really new when it happens.

“For example, when the [Federal Reserve] makes its announcement about monetary policy rates and the path of monetary policy going forward, we don’t always see a big market reaction,” said Indarte. “Sometimes mortgage rates or stock prices don’t move a whole lot.”

Take the analogy just a hair further: When markets don’t move a whole lot on what otherwise would be big news, it means Wall Street has a pretty good recipe for what the future market is going to look like.

“What are the ingredients here? That would be the data that would be things like job reports, the latest inflation numbers,” Indarte said.

Right now, traders are baking in the January jobs report, the latest consumer price index, the personal consumption expenditures price index, and tons of other data points they might use to, say, take a guess at what the Fed is going to do in March at their next interest rate-setting meeting.

And all those ingredients taken together? When mixed, they make a forecast. And that’s kind of like the batter, Indarte said. So long as they get the batter right, when the Fed announces interest rates, there’s not going to be a big market reaction.

But, as anyone who’s baked can probably relate to, sometimes you get the batter wrong.

“If we forgot a crucial ingredient, maybe if we overlooked house prices, then our cake might fall flat,” Indarte said.

Get the ingredients wrong or leave one out, and what comes out of the oven might be a surprise. It happened at the beginning of the pandemic: Nobody had an emergency interest rate cut on their list of ingredients in March 2020, and traders reacted with extreme volatility.

But there’s nuance, too. Sometimes it’s not that you’ve got the wrong ingredients, it’s that the measurements aren’t right.

“You could have the same people looking at the same information, but if we can’t agree on how to put that information together, if we have different narratives about the significance of the jobs numbers versus consumer sentiment and so on, we can come up with different forecasts,” Indarte said.

And lately, between government shutdowns that have delayed the release of data reports and staffing cuts at the very agencies that produce those reports, we’re kind of just eyeballing the ingredients.

“If you don’t have a complete recipe — maybe you have all the right ingredients in front of you, but you don’t know the proportions,” said Indarte. “You might have had a chance to get to the right recipe, but if you’re if you’re missing maybe the knowledge or skills in order to get there, then it might not work out.”

That’s all to say, a cake is only as good as its recipe and a forecast is only as good as its parts. At the end of the day, it’s all about the quality of the ingredients.

Market place

Analytics

How China can survive without the Strait of Hormuz

The world’s largest importer of oil through the Strait of Hormuz is, paradoxically, also one of the best placed to weather the waterway’s closure.

China consumes oceans of oil from the Gulf and imports roughly as much from the region as India, Japan and South Korea combined. In response to the closure of the Strait, officials across Asia are asking citizens to take shorter showers or work from home to save energy. In China, the ruling Communist Party’s flagship newspaper is instead telling readers the country holds its own “energy rice bowl.”

While the editorial does not mention that Beijing has unofficially banned fuel exports to conserve supplies, the country is nonetheless more insulated than many of its neighbours thanks to years of policy measures that have reduced its vulnerability to energy shocks.

China boasts an electric vehicle fleet about as large as the rest of the world’s combined, vast and growing oil stockpiles, diversified supplies of oil, and gas and an electricity grid that is almost insulated from imports thanks to domestic coal and renewables.

“The current situation is really close to what Chinese planners have had in mind for decades,” said Lauri Myllyvirta, co-founder of the Centre for Research on Energy and Clean Air in Finland.

“It validates the drive to reduce reliance on seaborne fossil fuels.”

The unexpected EV boom

In late 2020, Beijing issued a goal for electric vehicle purchases to hit 20% of new sales in 2025. By last year, sales hit half of all new vehicles.

That unexpected boom in EVs means China’s fuel consumption has topped out after decades of breakneck growth. The country is burning and importing less oil than it was expected to just a few years ago.

Oil displaced by EVs last year was roughly equal to what China imported from Saudi Arabia, according to estimates from the Centre for Research on Energy and Clean Air.

The EV boom means China imports much less oil

Annual oil consumption displaced by electric vehicles in China

An insulated electricity grid

China’s electricity grid is powered almost entirely by coal and rapidly growing renewable energy. The boom in clean energy, which has exceeded Beijing’s own targets, is such that almost all the extra power the economy requires each year is met with new solar or wind. That means fewer coal imports and less liquefied natural gas (LNG) imported into the handful of coastal provinces where it is part of the electricity mix.

Lots of oil, but many suppliers

China imports lots of oil, but in contrast to other major Asian importers, it is careful to stay independent of any one supplier.

Take Japan: Tokyo normally buys nearly 80% of its oil from Saudi Arabia and the United Arab Emirates. China bought the same share of oil from eight countries, including large amounts of discounted oil from Russia, Venezuela and Iran, which U.S. sanctions place off limits for most buyers.

China keeps its oil imports diversified

Crude oil import volumes by origin for major importers. Less than 20% of China’s oil imports are from any one source.

China also funnels a share of those imports into the storage tanks of its secretive strategic petroleum reserve. No one knows exactly how big the reserves are, but combined with stocks held by commercial refiners, China has enough oil in storage to replace imports via the Strait of Hormuz for perhaps seven months by some estimates.

China has enough oil stored to cover seven months of imports via Hormuz

Domestic production is growing

China produced 4.3 million barrels per day of oil last year, a new record that was equal to about 40% of all oil imports. However, oil reserves are drying up and China is unlikely to replicate the U.S. shale oil boom.

Gas, however, is another story. Domestic production is growing fast enough that, combined with gas imported via pipeline, China is actually importing less LNG than it did in 2020.

China’s pipeline network allows it to diversify away from seaborne imports and source oil and gas from Russia, central Asia and Myanmar. Ambitious plans have been proposed for another Russian-China pipeline, the Power of Siberia 2, however it remains years from completion.

China’s pipeline gas imports have steadily risen since the Power of Siberia

Island neighbors such as Japan or Korea do not share the same geographic advantage

A more secure future

For decades China’s growth has been fueled by fossil fuels imported from overseas, in particular crude oil. But thanks to the EV boom, China is unhitching its growth engine from foreign oil.

“China’s oil demand is likely to peak this year and decline thereafter,” said Chen Lin, vice president of oil and gas research at Rystad Energy. “So although the import share will remain high, the situation is unlikely to worsen.”

Reuters

Analytics

Saudi Arabia to burn more oil for power this summer

Saudi Arabia is expected to burn more imported fuel oil for power generation this summer following a loss of natural gas supply from oilfields that have been shut after the Iran war curbed its oil exports, analysts said.

The rise in fuel oil use at power plants just as electricity demand jumps for cooling in the summer marks a setback for the kingdom’s push to switch to cleaner fuels.

The world’s top oil exporter has been forced to shut more than 3 million barrels per day of oil production after an Iranian blockade on the Strait of Hormuz halted crude exports from Ras Tanura, which in turn has reduced output of gas released with oil production.

Gas output slipped to 10.5 billion cubic feet per day (bcfd) in the first quarter, from 10.7 bcfd in the fourth quarter of 2025, despite the start-up of the Jafurah gas field in December, Saudi Aramco (2222.SE), opens new tab said in its latest quarterly earnings report.

To replace gas at power plants, Aramco ramped up fuel oil imports to about 1.7 million tons (360,000 bpd) in April, up 86% on-year, Vortexa data showed, with most of these imports discharged at terminals linked to power and desalination plants including Jeddah South and Shuqaiq Steam.

“The sharp increase in fuel oil imports is a leading indicator that oil burn will rise above year-ago levels,” Rahul Choudhary, vice president, oil & gas research at consultancy Rystad Energy, said.

The kingdom’s power demand typically rises from April and peaks in August, boosting crude, high-sulphur fuel oil (HSFO) and gas use at power plants.

The burning of crude and fuel oil for power could breach 1 million barrels per day this summer, countering efforts to switch to more gas and renewables and undoing the 991,000 bpd low seen in 2025, Choudhary said.

Saudi Aramco declined to comment. The Saudi government communications office did not respond to a request for comment.

ARAMCO PRIORITISES CRUDE FOR EXPORTS

Saudi Aramco is expected to burn less crude for power this summer as it prioritises crude, mostly Arab Light, for export via the East-West pipeline to the Red Sea port of Yanbu and as HSFO is cheaper than Saudi crude, analysts said.

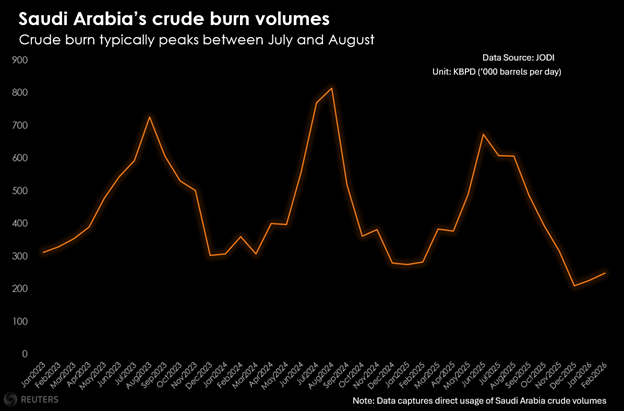

Last year, Saudi Arabia’s direct crude burn averaged 593,500 barrels per day (bpd) between June and September, data from the Joint Organisations Data Initiative (JODI) showed.

Crude burn typically peaks between July and August

Analysts’ views vary on how much crude Saudi Arabia will burn for power generation this summer.

Wood Mackenzie expects a 5,000 to 15,000 bpd drop in crude burn from an average of 629,000 bpd in June to August 2025.

“Every barrel of Arab Light crude burned domestically represents a significant loss in windfall export revenue,” said Jayadev D, oil research analyst at WoodMac.

Rystad Energy expects crude consumption for power to average about 540,000 to 550,000 bpd this summer.

“However, if the Hormuz disruption deepens or extends well into Q3, Aramco may pivot from substitution to direct crude burn as a contingency,” Choudhary said.

Koen Wessels, head of demand at Energy Aspects, expects Saudi Arabia to burn more crude this summer than in 2025 as it is constrained by how much crude supply it can divert to Red Sea ports.

Energy Aspects expects Hormuz transits to remain disrupted through the end of May, with a 50% recovery on pre-war tonnage in June, 60% in July and 70% in August, Wessels said.

Thomson Reuters

Analytics

How Much People Save Around the World

This chart ranks household savings rates across major economies using the latest OECD data. It reveals a wide gap between top savers and those struggling to set money aside. In countries like Sweden and Hungary, households save more than 10% of their income. In the U.S., that figure is just 4.9%.

In some cases, the gap is even more striking. Americans save roughly half as much as households in Mexico, highlighting how cost pressures and consumption patterns differ across economies.

How Much People Save by Country

Sweden ranks as the most disciplined saver, with net household savings rates rising nearly eightfold from 2.3% to 16% over the past two decades.

Many European countries also rank at the top of the list. Households continue to set aside a relatively large share of their income, including Hungary (14.3%) and France (12.8%). These elevated rates are often linked to structural factors such as pension systems and aging

he table below shows savings rates by country in 2024, or the latest available data:

| Country | Net Saving Rate (% of net disposable income) |

| 🇸🇪 Sweden | 16.0% |

| 🇭🇺 Hungary | 14.3% |

| 🇨🇿 Czechia | 13.7% |

| 🇫🇷 France | 12.8% |

| 🇦🇹 Austria | 11.7% |

| 🇩🇪 Germany | 11.2% |

| 🇳🇱 Netherlands | 9.5% |

| 🇪🇸 Spain | 9.2% |

| 🇮🇪 Ireland | 9.0% |

| 🇩🇰 Denmark | 8.5% |

| 🇲🇽 Mexico | 8.1% |

| 🇧🇪 Belgium | 6.6% |

| 🇵🇱 Poland | 6.1% |

| 🇦🇺 Australia | 6.1% |

| 🇱🇺 Luxembourg | 5.0% |

| 🇨🇦 Canada | 5.0% |

| 🇺🇸 United States | 4.9% |

| 🇰🇷 South Korea | 4.8% |

| 🇬🇧 United Kingdom | 4.7% |

| 🇵🇹 Portugal | 4.5% |

| 🇫🇮 Finland | 4.3% |

| 🇮🇹 Italy | 4.2% |

| 🇳🇴 Norway | 4.2% |

| 🇱🇹 Lithuania | 3.8% |

| 🇪🇪 Estonia | 3.0% |

| 🇯🇵 Japan | 0.9% |

| 🇱🇻 Latvia | 0.0% |

| 🇿🇦 South Africa | -1.0% |

| 🇳🇿 New Zealand | -1.3% |

In the middle of the pack, savings rates drop off quickly. The U.S., Canada, and the UK all cluster around 5% or lower, far behind top European savers. The gap is particularly striking when compared globally. U.S. households save about half as much as those in Mexico, and less than one-third of what households in Sweden set aside each year.

At the bottom of the ranking, the picture flips entirely. In countries like New Zealand and South Africa, households are not saving at all. Instead, they are spending more than they earn.

Negative savings rates typically mean people are dipping into past savings or taking on debt to cover everyday expenses, a sign of financial strain rather than choice.

What It Means Going Forward

Savings rates are a key signal of financial resilience.

Countries where households consistently save more tend to have a stronger buffer against inflation, job losses, or economic shocks. Higher savings can also support long-term investment and stability.

On the other hand, persistently low or negative savings rates can point to underlying pressure. When households have little margin to save, economies may become more vulnerable to downturns, rising debt levels, and weaker consumer spending over time.

Visual Capitalist

King Fahad National Library Selects Face to Face with ISIS as “Book of the Day”

Fakeeh Health Achieves National Institute for Health Specialties (NIHS) Institutional Accreditation for Residency Training

White and Black Events & PR Announces New Expansion Phase Led by Nagham Amer, Including Regional Market Growth and the Launch of a Skincare Brand

UAE’s café culture keeps growing despite price pressure

Is February 2026 really a once-in -283-years MiracleIn?

Netflix to Livestream BTS Comeback Concert

-

UAE7 months ago

UAE7 months agoUAE’s café culture keeps growing despite price pressure

-

Discover6 months ago

Discover6 months agoIs February 2026 really a once-in -283-years MiracleIn?

-

Entertainment6 months ago

Entertainment6 months agoNetflix to Livestream BTS Comeback Concert

-

Football7 months ago

Football7 months agoAlgeria, Burkina Faso, Côte d’Ivoire win AFCON 2025 openers

-

politics3 months ago

politics3 months agoAraghchi, Oman Sultan discuss transit, stability in Muscat

-

Health7 months ago

Health7 months agoNMC Royal Hospital, Khalifa City, performs rare wrist salvage, restoring function for young patient

-

Health7 months ago

Health7 months agoBascom Palmer Eye Institute Abu Dhabi and Emirates Society of Ophthalmology Sign Strategic Partnership Agreement

-

Health8 months ago

Health8 months agoEmirates Society of Colorectal Surgery Concludes the 3rd International Congress Under the Leadership of Dr. Sara Al Bastaki